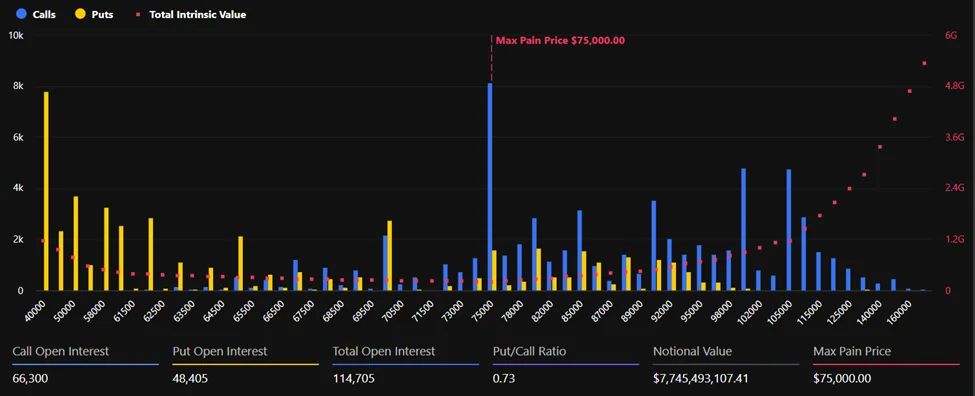

The biggest derivatives market event of February has arrived: a total of $8.72 billion worth of Bitcoin and Ethereum option contracts have expired. While the crypto markets are hovering at a delicate balance point with this critical development, both technical indicators and investor sentiment paint an interesting picture. Bitcoin accounts for the majority of this figure. With 114,705 contracts and a value of approximately $7.74 billion, BTC leads by a wide margin, while Ethereum has 478,992 contracts and a share of $975 million. This combined volume of the two assets represents approximately twenty percent of the total open positions; this makes the potential impact of the expiration on the market significant.

Maximum pain levels are creating pressure

Both assets are trading significantly below their "maximum pain" thresholds. This concept refers to the price level at which the greatest number of options become worthless. Bitcoin is trading at $68,052, approximately $7,000 below the $75,000 threshold, while Ethereum is hovering around $2,035, below the $2,200 threshold. Historical patterns suggest that spot prices tend to approach these levels before expiration; this could create upward pressure in the short term. In the options structure, call contracts outweigh put contracts. The buy/sell ratio is 0.73 for Bitcoin and 0.78 for Ethereum. While this theoretically presents an optimistic picture, it takes on a different form in terms of volatility indicators. According to Deribit data, Bitcoin's implied volatility index is at 87.7% of its historical range, while Ethereum's volatility is approximately 15-20 points higher than Bitcoin's throughout the entire expiration curve.

Anxiety persists in derivatives markets

Bitcoin managed to retest the $70,000 level in recent days; however, this recovery was not enough to alleviate the deep anxiety in the market. There was a net inflow of $764 million into licensed Bitcoin ETFs in the US in the last two days. While this figure partially offset the $1.2 billion outflow in the previous eight trading days, it did not revive the appetite for leveraged buying in the futures market. The fact that the Bitcoin futures premium is hovering well below the neutral threshold of 5%, at only 2%, confirms this picture.

What's behind the decline?

Questions remain unanswered regarding the main factor that caused Bitcoin to fall by 32% in eight weeks. It is known that the major crash in October led to a $19 billion forced liquidation, coinciding with the US tariff increases on Chinese goods. Binance's payment of $283 million in compensation to users, citing internal pricing errors, was also among the notable developments. On the other hand, the controversy deepened when an analyst from Jefferies removed Bitcoin from their model portfolio, citing the risks of quantum computing. In response, the developer community prepared the BIP-360 proposal, which aims for a transition to post-quantum cryptography, while some market participants viewed Jane Street's large positions in Bitcoin ETFs with curiosity and suspicion. With all these developments in mind, Bitcoin's monthly price movement was as follows: