While expectations for the end of the year are strengthening again in the Bitcoin market, data from the options side shows that investors are not exhibiting one-sided optimism. According to Deribit data, the open interest in Bitcoin options with a December 25 expiry date has reached $6 billion. While this figure initially points to a very strong bullish expectation, the details reveal that the picture needs to be read more balanced.

Bitcoin has gained approximately 33 percent in value since its year-to-date low of $60,130 on February 6th. This rise has brought more optimistic price targets for the end of the year back into the spotlight. In particular, the high open interest accumulated in call options above $115,000 has been interpreted as the market pricing in a strong upward possibility. However, high open interest in the options market does not always directly mean a price expectation.

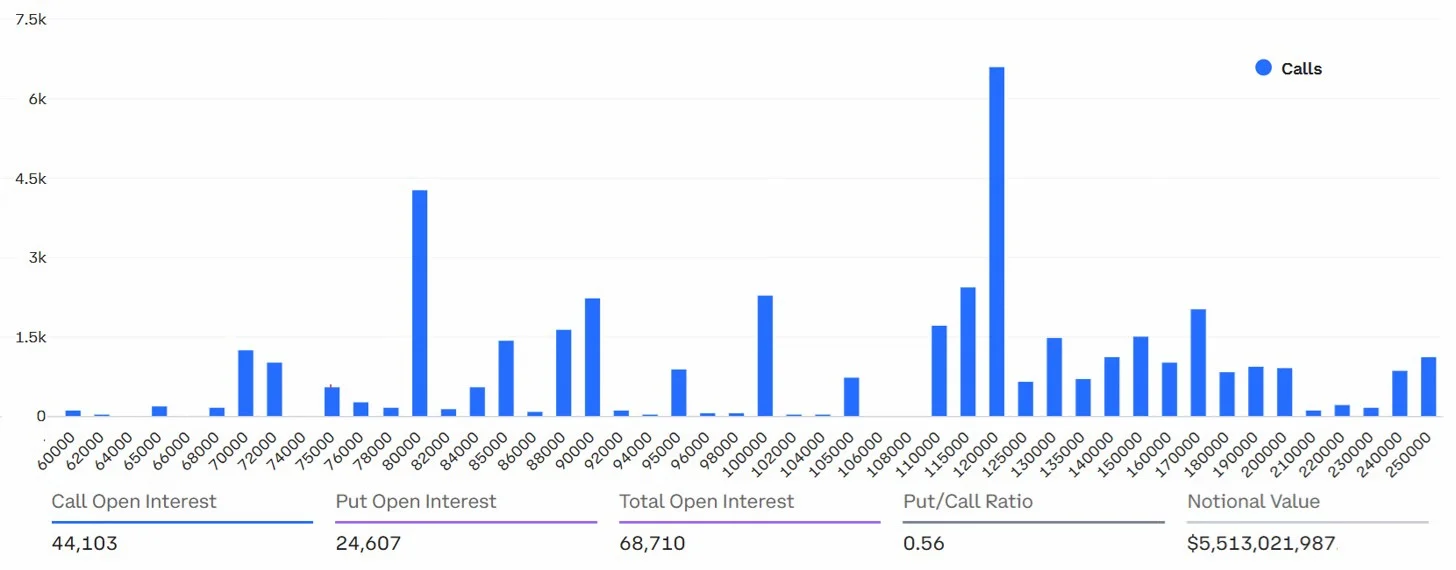

Deribit stands out in year-end options

Deribit's share in December Bitcoin options is quite high. With $5.5 billion in open interest, the platform holds approximately 92 percent of the total market in this area. However, the actual value at expiry may be much lower than the current open position size. This is because a significant portion of these positions are not opened for direct directional betting purposes, but rather as part of hedging or neutral strategies.

In the options market, investors don't just take simple positions betting on the price reaching a certain level. Strategies built with different expiries, different strike prices, and reciprocal positions can generate profit even if the price doesn't move sharply. Therefore, interpreting the $6 billion open position alone as "Bitcoin is definitely preparing for a major surge at the end of the year" doesn't seem healthy. Call options are dominant, but extreme targets exist on both sides.

At Deribit, put options remain 56% lower than call options. This trend in the put-call ratio is not surprising, given that investors in the crypto market are naturally more optimistic. Nevertheless, the fact that there are $1.85 billion in open positions in call options above $115,000 is noteworthy. This picture shows that Bitcoin investors are keeping quite high prices on the table for the end of the year. However, similarly, there is a significant accumulation of positions on the sell side for extreme scenarios. Open positions in put options below $55,000 reach approximately $1 billion. This reveals that a considerable amount of positions have been opened in price zones considered "low probability" on both the bull and bear sides.

In other words, concluding that the market is overly optimistic by only looking at call options may be incomplete. On the bear side, there is similarly positioning for sharply declining scenarios. The fact that approximately half of the open positions are tied to distant price targets on both sides shows that investors are not only making directional predictions but also trying to manage portfolio risk. Professional investors are pricing in downside risk.

One of the indicators that gives clearer signals in option pricing is the delta skew metric. This indicator measures how investors premium upside and downside risks. On Deribit, six-month Bitcoin put options are trading at a 9% premium compared to equivalent call options. In neutral market conditions, this indicator is generally expected to remain in the range of minus 6% to plus 6%. A 9% put option premium indicates that professional investors are cautious about a potential pullback in Bitcoin. While this doesn't signal panic in the market, it reveals that downside risks are not being ignored. The lack of significant relief in derivatives markets despite Bitcoin's recovery towards the $80,000 level is also important in this respect. High-strike call options, on the other hand, allow investors to participate in large bullish scenarios at a relatively low cost. For example, a call option with a strike price of $120,000 offers an investor the potential to profit if Bitcoin reaches much higher levels by the end of the year, at a limited cost. Such positions may be part of an asymmetric return quest rather than a direct expectation of a strong bull run. Therefore, interpreting the $1.85 billion high-price target call option position solely as excessive bullish confidence can be misleading. Interest in the Bitcoin options market for the end of the year is high, but professional investors are simultaneously seeking protection against downside risks. The market remains cautious while keeping the possibility of an uptrend on the table.