Traditional finance (TradFi) seeks access to the speed and efficiency of blockchain, but compliance, privacy, and auditability are indispensable. Rayls (RLS) emerges as an EVM-compliant and enterprise-focused blockchain ecosystem that responds to this need. Aiming to bring $100 trillion in liquidity and a population of 6 billion banked individuals into the digital world, Rayls offers financial institutions a compliant and scalable hybrid blockchain infrastructure. Let's take a look at what Rayls offers and why it's attracting attention in the financial world.

Rayls' Definition and Origins

Rayls is an Ethereum-compliant blockchain platform designed to bring together traditional finance and decentralized finance. This ecosystem allows financial institutions to securely tokenize assets such as deposits and bonds, manage them on their own private networks, and move them to global DeFi markets when needed. Thus, regulatory-compliant asset tokenization and interoperability between private networks and open chains are provided under one roof. Rayls' primary goal is to digitize at least $100 trillion worth of traditional financial liquidity and connect millions of customers of financial institutions with the advantages of blockchain. In doing so, it aims to address the biggest challenges of corporate finance, such as compliance, privacy, and transaction efficiency. For example, banks can convert their deposits into digital tokens on Rayls and use them for internal transactions, then transfer these tokens to the public chain via secure bridges when they want to access global liquidity. This transforms traditional finance (tradfi) activities into a cycle that fuels DeFi growth. Rayls' focus use cases include cross-border payments, tokenization of real-world assets (RWA), digital currency/CBDC projects, and corporate DeFi integrations. The platform enables financial institutions to make fast and low-cost payments 24/7, while allowing complex financial products (bonds, loans, fund shares, etc.) to be tokenized and made accessible to global liquidity. Rayls is also designed for use in central bank digital currency (CBDC) pilots and major interbank reconciliation projects. The fact that Rayls' privacy technology is already being used in the Brazilian Central Bank's Drex pilot and showcased as a cross-border payment solution at global events such as the G20 TechSprint demonstrates the practical application of these focus areas.

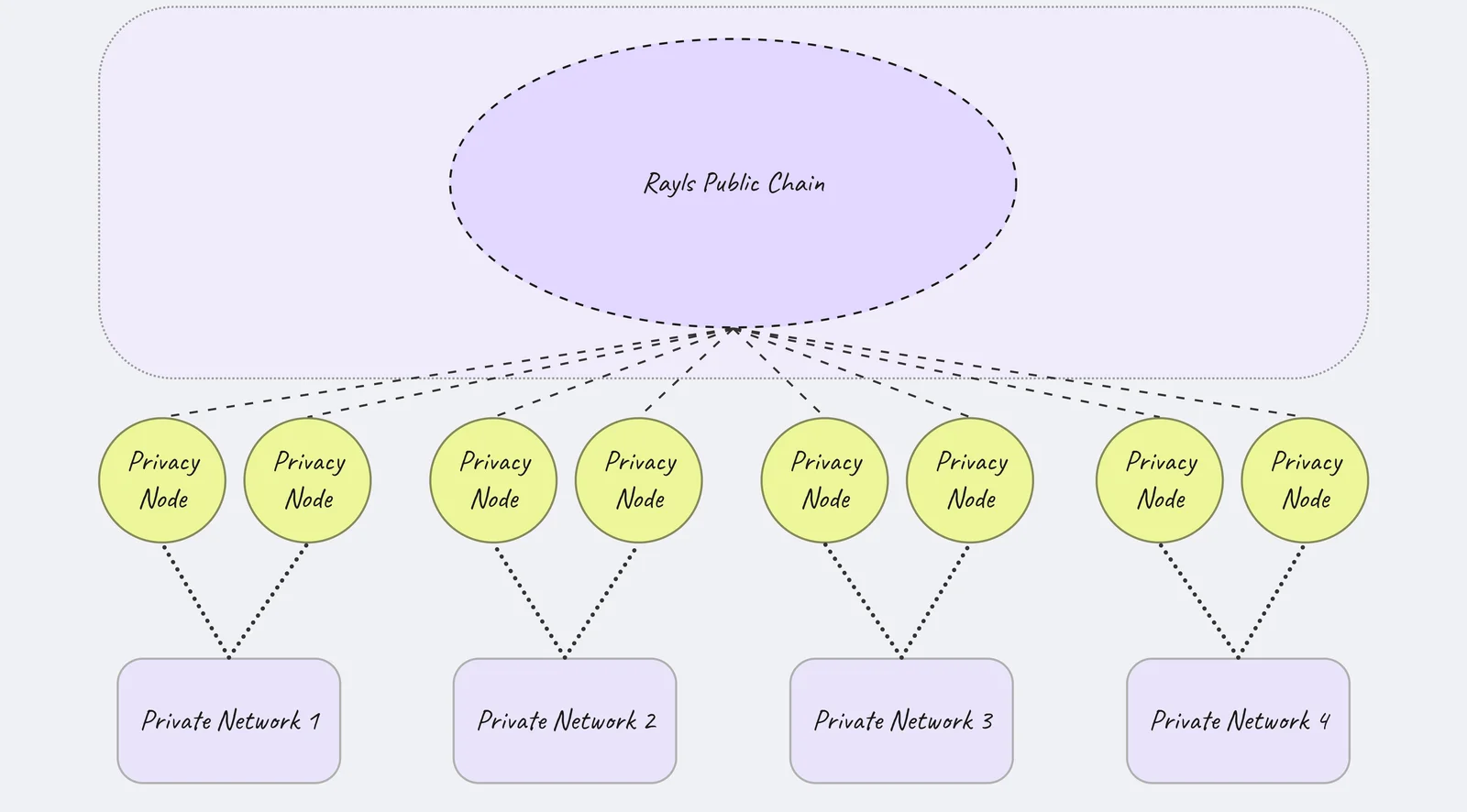

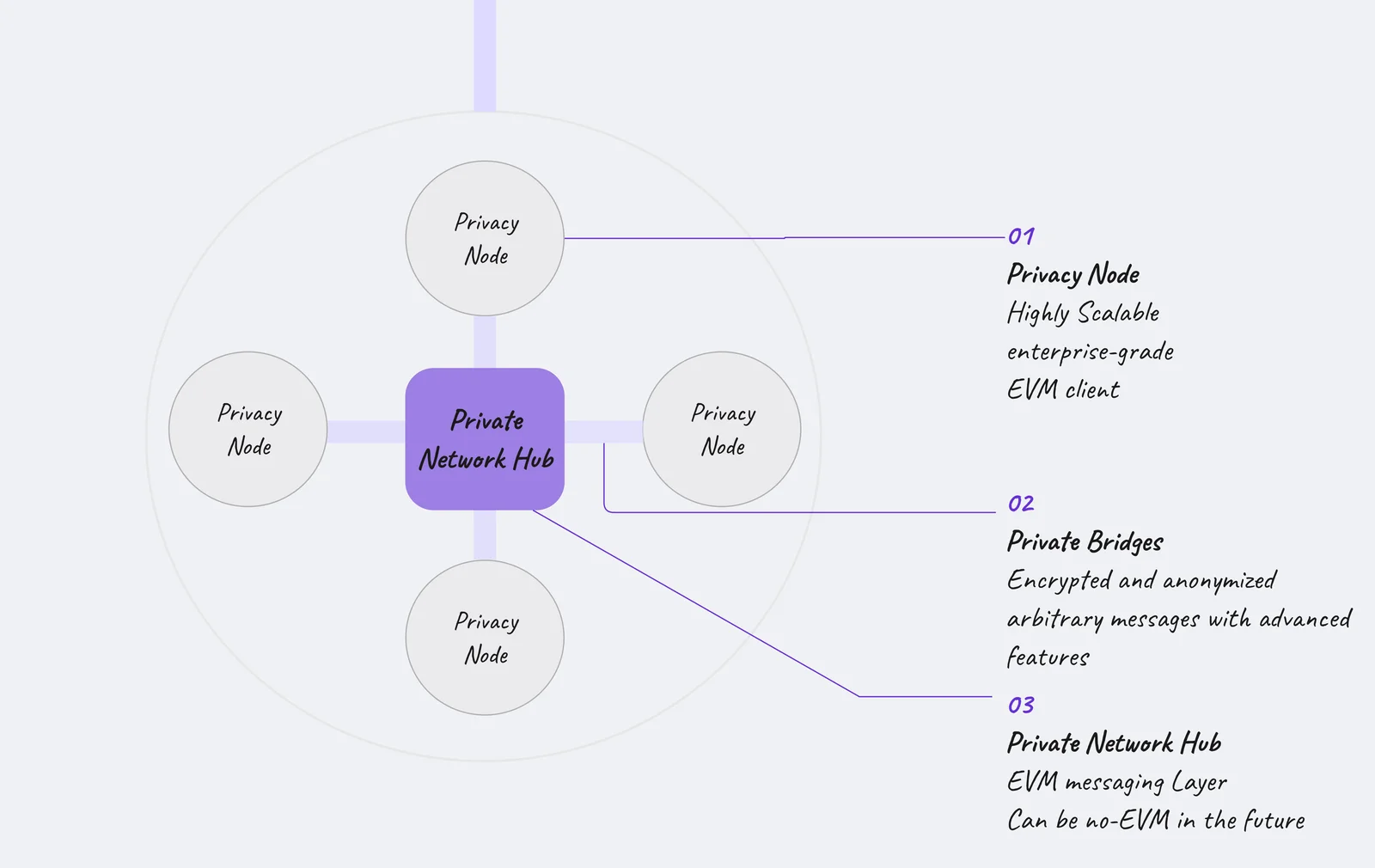

Rayls stands out with its unique hybrid architecture. The system consists of a combination of a public blockchain (EVM-compliant, permissionless) called Rayls Public Chain and permissioned private subnets called Value Exchange Networks (VEN). Each financial institution can conduct its transactions in complete privacy by running its own private EVM sub-chain (VEN); these sub-chains provide high privacy to participants thanks to zero-knowledge proof-of-stake (ZK) and fully homomorphic cryptography technologies. At the same time, each VEN is connected to Rayls' public chain via secure bridges, and assets can be moved to the public chain when needed. This approach offers each institution infinite scalability (since each institution maintains its own ledger) while allowing all networks to meet in a common liquidity pool.

Rayls places regulatory compliance at the heart of its design. All participants who will transact on the network are required to undergo KYC (know your customer) verification beforehand. This prevents malicious or sanctioned addresses from infiltrating the system, even though the Rayls Public Chain is open to everyone. In addition, Rayls meets institutional regulatory expectations with its integrated AML (anti-money laundering) logic, traceable but private transaction structure, and auditable smart contracts. Thanks to high transaction speed and predictable low gas fees, institutions can perform the slow and costly reconciliation processes in their traditional systems in seconds and transparently on Rayls.

Rayls History: Key Milestones

Rayls doesn't have a very long history as it is a new cryptocurrency project. However, you can see the coin's milestones below:

Project Introduction: Developed by Parfin company under the name Parchain, Rayls was introduced to the public in July 2024 with an enterprise UniFi blockchain vision. The London and Brazil-based Parfin team announced this project after two years of R&D work with leading banks around the world.

Testnet Launch: In April 2025, the first public testnet, Steam Testnet, was launched. During this phase, KYC onboarding, MetaMask wallet integration, and basic authentication tools were implemented. In June 2025, the testnet gained multi-wallet support and mobile access capabilities, making it ready for user testing.

Privacy-Focused Architecture (MagLev): Between July and September 2025, Rayls reinforced its privacy and compliance-focused architecture through the MagLev Testnet. In July, a customized sequencer and a zkTLS-based digital authentication system were integrated, enabling KYC verification without sharing public banking data. By September, enterprise features such as a private bridge, advanced AML logic, custody modules, and sponsored trading were added to the network. These innovations solidified the secure transition between private enterprise networks and the programmable public chain.

Token Launch (TGE): In November 2025, Rayls matured by testing final features supporting staking and public chain transactions on its public network. Subsequently, on December 1, 2025, the Token Generation Event (TGE) was held, and a total of 1.5 billion RLS tokens were made public. From this date, the RLS token began to be listed on leading exchanges. This provided token access for users and institutions who joined the Rayls ecosystem early.

Institutional pilots and collaborations: Rayls technology began to demonstrate its capabilities in real-world applications. The Central Bank of Brazil selected Rayls' privacy solution for its pilot project for the country's digital currency, Drex, highlighting its commitment to institutional blockchain security. At the same time, Rayls was showcased as an innovative solution in the global payment infrastructure field with its CBDC and tokenized deposit integration at the G20/BIS TechSprint 2023 event and won an award in the competition. These developments led to Rayls gaining international recognition, and the project gained strength towards the end of 2025 by securing strategic investments from major players such as Tether, Mastercard, and Accenture.

December 2025: RLS coin is trading around $0.015 by the end of December 2025.

Why is Rayls Important?

Rays is seen as a critical infrastructure bridging the gap between corporate finance and the blockchain world. It offers significant advantages in terms of the innovations it brings to both banks and financial institutions, as well as regulators:

Use Cases

Tokenization of real-world assets: With Rayls, classic financial assets such as corporate bonds, bank deposits, loan portfolios, trade receivables, or mutual fund shares can be converted into digital tokens. These tokens are initially held and managed confidentially in the banks' own private ledgers, and if desired, can be shared with trusted partners for multi-party transactions. Then, when liquidity or investor access is needed, they can be moved to public chains and traded. Thus, previously illiquid or difficult-to-divide assets become easily bought and sold with Rayls. This use case means new revenue opportunities and more flexible investment products for banks, asset managers, and funds.

Cross-border payments and reconciliation: Rayls aims to complete interbank payments and large-scale reconciliation transactions in seconds instead of days. Institutions can make 24/7 real-time value transfers between financial networks in different countries thanks to Rayls' hybrid structure. For example, two banks can prepare transactions on their own private Rayls networks and instantly transfer them to the counterparty's network via the Rayls Public Chain. Since transactions are confidential but verifiable, a fast and compliant cross-border payment infrastructure is created. This provides an alternative to the slowness and high cost of traditional systems like SWIFT, resulting in efficiency in global payments.

CBDC and digital currency issuance: Central banks and commercial banks can issue their own digital currencies or tokenized deposit products on Rayls. Since Rayls' design includes privacy and smart contract-based rule sets, for example, when a central bank issues a CBDC (Central Bank Digital Currency) using the Rayls infrastructure, it can both track transactions and protect the privacy of citizens. Large interbank payments or securities swaps can also be made on the Rayls network in accordance with delivery-for-payment (DvP) principles, minimizing risk. The Brazilian Central Bank's use of Rayls in its Drex pilot is a concrete demonstration of the potential in this area.

DeFi applications and smart contracts: Rayls opens doors to the existing DeFi ecosystem because it is Ethereum compatible. Solidity smart contracts can be run on the Rayls Public Chain; protocols like Uniswap and Aave can be re-implemented on Rayls while meeting KYC requirements. Developers can both develop dApps on a platform that can reach institutional clients and attract institutional liquidity to these applications. For example, a lending protocol running on Rayls can accept bank-tokenized loan portfolios as collateral. Rayls' privacy and compliance layers come into play when necessary, ensuring that such DeFi transactions are conducted within the rules. As a result, DeFi applications built on Rayls can accommodate far more asset types and participants than traditional finance.

Institutional private networks and collaborations: Rayls' permissioned subnet (VEN) structure facilitates the creation of a shared blockchain network among multiple financial institutions. For example, a consortium of several banks could create a shared private network on Rayls and conduct securities trading or clearing transactions among themselves within this network. Each institution maintains full control and data privacy on its own node, while the shared network accelerates multi-party consensus. This model offers significant advantages in interbank collateral management, internal liquidity sharing, or shared KYC/AML processes. Rayls' features, such as role-based authorization and auditor views, allow these private networks to operate flexibly and in compliance with regulatory requirements.

Token Economy

Supply and Distribution: The total supply of Rayls Token (RLS) is set at 10 billion units. 15% of this amount was released during the Token Generation Event on December 1, 2025, while the remaining tokens were distributed among the foundation, team, investors, and ecosystem development funds, tied to specific vesting schedules. In this way, tokens that are not in circulation will be released in a controlled manner over time to maintain supply balance. Usage and Fees: RLS token is the central transaction token of the Rayls ecosystem. Both gas fees for smart contract transactions on the Rayls Public Chain are paid with RLS, and RLS is used as a utility token in transactions such as asset creation, transfer, and exchange on private institutional networks. For example, when a bank issues a new token on Rayls or two institutions exchange assets on the private network, they pay transaction fees with RLS. Thus, as activity on the network increases, the demand for RLS also increases. Additionally, RLS is designed as a common payment unit for other services on the network, such as custody services and bridging operations.

Burning mechanism (deflation): Rayls aims for a deflationary token economy. A certain portion of the transaction fees on the network (currently 50%) is burned and removed from circulation. This mechanism directly links network usage to the scarcity of RLS tokens; the more intensively the network is used, the more tokens are burned, and over time the circulating supply decreases. For example, if transaction volume increases with increased institutional adoption, the amount of tokens burned will also increase, contributing to RLS becoming more valuable in the long run. The deflation model also supports the sustainability of the token economy by curbing speculative inflation.

Staking and validators: The Rayls network is secured with a proof-of-stake (PoS)-like consensus model. The network's validator nodes are mostly selected from financial institutions or approved organizations, and these validators are required to stake (lock) a certain amount of RLS for the security of the network. RLS token holders can contribute to network security by delegating their tokens to existing validators without becoming validators themselves, and in return earn staking rewards. This model encourages a broad institutional consensus structure while also offering passive income opportunities to individual token holders. Since staked tokens are at risk of slashing in case of malicious behavior, network security is supported by economic incentives.

Governance and ecosystem: Although the Rayls network is initially developed and managed by the Rayls Foundation, a transition to a community-driven governance (DAO) model is planned in the long term. As the number of validators and community participation increases, RLS token holders will have voting rights in decision-making processes regarding the future of the network. For example, issues such as network upgrades, block reward parameters, the addition of new features, or the distribution of ecosystem funds may be put to a vote by RLS holders in the future. Until this transition, the Rayls Foundation is implementing a centralized governance model to guarantee the security and compliance of the network. In addition, approximately 35% of the RLS token supply is reserved for ecosystem incentives (developer grants, liquidity programs, community rewards, etc.). This fund will be used to support those developing applications on Rayls, organizations using the network, and community contributions, thereby encouraging the growth of the ecosystem.

Who Founded Rayls?

Parfin, the core development company behind Rayls, was founded in 2019 by Marcos Viriato and Alex Buelau, based in London and Rio de Janeiro. The Parfin team, a multidisciplinary group of engineers, cryptographers, and bankers, worked with some of the world's largest financial institutions for over two years to develop the Rayls project. Initially codenamed "Parchain," Rayls was rebranded as Rayls in 2024.

Marcos Viriato is the CEO of Parfin and one of the leaders of the Rayls project. A former investment banker and early adopter of blockchain, he shapes Rayls' corporate finance vision. Alex Buelau, as Parfin's CPTO (Chief Product & Technology Officer), is responsible for Rayls' technical architecture. Active in the crypto sector since 2013, Buelau brings his extensive experience, from mining to investing, to Rayls. The team consists of over 90 expert engineers, along with executives (such as CCO Bruno Cavalin and CDO CH Lopes) who have more than 20 years of experience in finance and technology. Rayls' founding team operates with the mission of "building the financial infrastructure of the future." Marcos Viriato and his team's core vision is based on the belief that digital assets and blockchain technology are not a passing fad in the financial world, but a permanent and transformative force. In line with this vision, Parfin/Rayls develops enterprise-level products that enable financial institutions to access digital assets securely and efficiently. Specifically for Rayls, the goal is to integrate the innovative opportunities of blockchain into the financial sector without compromising the compliance and security required by banks and regulators. In other words, to provide an infrastructure that we can call the internet of value for the use of the corporate world. Although Rayls is still a new ecosystem, it has a strong corporate support network behind it. The project started by incorporating Parfin's existing customer base—large financial institutions and fintech companies—(prior to Rayls, Parfin provided custody and digital asset services to banks like Itaú and Santander in Latin America). Global financial giants like Mastercard and Accenture also provided strategic support to the project by investing in Rayls' vision. One of the investments received in 2025 was from stablecoin issuer Tether, which allowed Rayls to integrate a market-leading stablecoin like USDT into Latin American institutions. Within the ecosystem, local players like Núclea (Brazil's largest financial market infrastructure company) are also developing institutional tokenization solutions using the Rayls network. On the community side, Rayls, with its phased decentralization approach, is trying to attract developers and users with incentive programs while establishing regular feedback loops with institutional participants. As a result, the Rayls ecosystem; It has a unique mix of banks, central banks, institutional investors, technology partners, and regulators.

Frequently Asked Questions (FAQ)

Below you will find some frequently asked questions and answers about Rayls:

What is the relationship between Rayls and the Ethereum network?: Rayls is a network compatible with the Ethereum Virtual Machine (EVM), so it can integrate with smart contracts and tools in the Ethereum ecosystem. However, Rayls operates its own independent blockchain; it connects the private Rayls network with the public Rayls chain by adopting an Ethereum L2 (sidechain) architecture. In this way, it accesses Ethereum's extensive liquidity and protocol ecosystem while creating a "clean" and compliant DeFi environment by implementing additional rules and improvements such as KYC on its own network.

Is KYC mandatory on the Rayls network?: Yes. KYC (Identity Verification) is mandatory for all users and institutions who want to participate in the Rayls ecosystem and conduct transactions. Any wallet address on the Rayls Public Chain must prove its legal compliance with decentralized identity verification before the first interaction. This practice provides a secure environment for institutions by purging the network of malicious actors and forms the basis of Rayls' vision of transparent yet regulated DeFi.

Why do corporate companies use Rayls?: Rayls addresses the needs of corporate finance by offering fast deployment, low cost, and a high level of privacy. For example, banks can process cross-border payments in seconds with Rayls, thus improving their liquidity management. At the same time, thanks to integrated KYC/AML controls and encrypted transaction infrastructure, transactions are both automated and remain open to regulatory oversight. As a result, organizations gain operational efficiency, accelerate reconciliation processes, and become able to offer new digital asset services (e.g., tokenized deposits, digital bonds) by using Rayls. These advantages make Rayls particularly attractive for large banks, asset managers, and fintech companies.

When will the Rayls mainnet be operational?: The Rayls project's mainnet V1 version is planned to be launched in the first quarter of 2026. Throughout 2025, Rayls went through various testnet phases, and the public distribution of the RLS token was completed in December 2025. With the activation of the mainnet, enterprise privacy nodes will begin operating at full capacity, and Rayls will be ready for enterprise-level production use. According to the roadmap, the integration of the Enygma privacy protocol into the public chain and improvements supporting multi-network connectivity with different networks are also targeted for 2026.

Can individual users use Rayls?: Rayls is primarily a platform designed for enterprise use. However, individual users (if they complete the relevant KYC processes) can also transact on the Rayls Public Chain and access Rayls-based applications. The fact that all users have undergone identity verification ensures that individuals and institutions can interact securely on the same network. However, it should be emphasized that the Rayls network is not focused on the average end-user; in its current form, it is largely shaped according to the needs of institutions such as banks and fintech companies. While individual investors can indirectly participate in the ecosystem through exchanges listing the RLS token, directly using the Rayls network may require interfaces and processes developed for institutions.

Discover the latest analyses, reviews, and guides on Rayls and the enterprise blockchain ecosystem in the JR Crypto Guide series.

#what is ralys#what is rls coin#rls coin price#rayls coin#rayls#rayls tokenomics#how does rayls work#rayls rwa

Do you have any questions?Feel free to send us your questions or request a free consultation.