Curve DAO Token (CRV) holds a significant place in the DeFi ecosystem as the governance token of the Curve Finance protocol. To briefly define Curve Finance, it is an Ethereum-based automated market maker (AMM) protocol focused on stablecoin trading. Liquidity pools on Curve enable exchanges between assets of similar value with minimal price slippage.

CRV coin is the governance and reward tool of this system. So, the answer to the question "What is CRV coin?" is that it is a token that offers participation in decision-making processes within the Curve ecosystem and incentivizes liquidity providers.

Developed in 2020 under the leadership of Russian physicist and software developer Michael Egorov, Curve was created to enable low-cost and low-volatility transactions between stablecoins. This vision has made Curve a reliable infrastructure for both DeFi users and large investors. In this guide, we will address all the questions such as when the Curve DAO Token (CRV) was introduced, how it works, what functions it serves, and what its position in the DeFi ecosystem is.

Definition and Origins of the Curve DAO Token

The Curve DAO Token (CRV) is the governance token of Curve Finance, a decentralized exchange prominent in the DeFi ecosystem. CRV's primary purpose is to incentivize liquidity pools on Curve and make protocol governance community-based.

Curve DAO launched in August, during the hot summer of 2020, during the DeFi boom. An interesting detail: just before the official launch, an anonymous developer deployed Curve's smart contracts, launching the CRV token a day earlier than expected. The Curve team confirmed this event and recognized August 14, 2020, as CRV's birthday.

The total maximum supply is approximately 3.303 billion CRV. Approximately 43% of this, or 1.3 billion CRV, was allocated to locked distribution and vesting programs; in the early days, there was virtually no CRV in circulation.

The project's development team consists of an experienced team led by Russian-born physicist and software developer Michael Egorov. Egorov has a strong background in cryptography, having previously participated in projects like NuCypher. The Curve protocol launched in January 2020, launching the first stablecoin pool on Ethereum and becoming the first AMM platform specifically optimized for stablecoin exchanges.

CRV token inflation plan. Source: CRV whitepaper

The Curve DAO Token's launch objective was to bring a new dimension to the concept of liquidity pools in DeFi. Unlike general-purpose AMMs like Uniswap, Curve focused on the exchange of assets of similar value (e.g., stablecoins pegged to $1). This structure allowed users to trade between stablecoins with near-zero slippage and benefit from low fees.

The CRV token serves as both governance and an incentive tool to ensure the sustainability of this model. CRV holders can vote on key issues such as the protocol's fee structure, the addition of new pools, and the distribution of liquidity rewards. This puts control and the future of Curve in the hands of the community rather than a central team.

The Curve DAO Token's History: Key Milestones

Since its launch, the Curve protocol and CRV token have experienced several critical milestones in the DeFi ecosystem. A look at the history of Curve coin reveals some notable developments:

January 2020: Curve Finance launched its first liquidity pool on Ethereum (cDAI–cUSDC pool). This marked the birth of the first stablecoin-focused automated market maker (AMM) protocol.

August 2020: The CRV token and Curve DAO were officially launched. The total supply was set at 3.03 billion CRV, approximately 1.3 billion of which were allocated to locked distribution programs. On launch day, the CRV price briefly surged above $50 (some sources say it briefly reached $60), but by the end of the same day, it had fallen to around $10. Within the first weeks, the price had fallen below $1.

September 2020: A revenue sharing system based on community votes was implemented. Now, 50% of Curve's transaction fees were distributed to users who locked their CRV tokens and deposited them into the governance contract. Thus, CRV stakers began receiving a share of the platform's revenues. The famous 3pool pool, comprised of DAI, USDC, and USDT, was also launched during this period.

Late 2020: Curve DAO introduced the "vote-escrowed CRV (veCRV)" system. CRV holders began earning veCRV by locking their tokens for a certain period of time. This model incentivized users for long-term governance by granting greater voting power and a share of revenue to long-term locking. Later that year, a community decision approved transferring half of transaction fees to veCRV holders, officially marking the beginning of the era of sharing protocol revenues.

2021: Curve began transitioning beyond Ethereum to a multi-chain architecture. In January, integration with the Avalanche and Harmony networks was achieved, and in February, Curve was now available on the Fantom network. In April 2021, it was deployed on Polygon (Matic) and received liquidity incentives from the Polygon team. In July, pools were opened on the Ethereum sidechain xDai, and the Arbitrum integration was completed in August. That same month, Curve's total asset lockup (TVL) surpassed $10 billion for the first time. This expansion has made Curve a key provider of stablecoin liquidity across multiple ecosystems.

Summer 2021: With the rise of the DeFi market, the CRV token experienced a strong rally. In August, the price reached around $6.50, marking an all-time high. Some sources indicate that it briefly reached $6.74 in January 2022.

2022: Despite the market decline, the Curve team continued its development without slowing down. The CRV burn mechanism and revenue sharing model were updated through community votes. Some proposals envisioned using a portion of management fees to buy back and burn CRV from the market, aiming to limit the growth rate of the circulating supply. In January 2022, Curve broke records with $24.3 billion in total locked value and launched on the Moonbeam (Polkadot ecosystem) and Aurora (Near ecosystem) networks. During the Terra ecosystem's collapse in May, Curve pools reached a daily trading volume of $5.8 billion. That same year, Curve's web domain (curve.fi) was subjected to a DNS attack, but the team quickly contained the incident. By the end of the year, the CRV price was fluctuating between $0.40 and $1.

2023: The Curve ecosystem gained its own stablecoin, crvUSD. Launched in May, crvUSD was designed as an over-collateralized stablecoin where users could borrow by providing collateral. Thanks to the LLAMMA (Lending-Liquidating AMM) algorithm, liquidations occur gradually, providing a more stable experience for borrowers. In July 2023, Curve was shaken by a major security incident. A vulnerability in the Vyper language led to the hacking of some pools, and approximately $70 million worth of crypto assets were stolen. This incident dropped the CRV price from $0.73 to $0.62. Founder Michael Egorov's highly collateralized loans on Aave faced liquidation risk, but with the support of the DeFi community and major players like Convex, Frax, and Aave, the situation was brought under control. After the incident, the Curve team tightened its security controls and reconsidered its contracts.

2024: Following the hack, Curve entered a restructuring process. Emergency measures were implemented through community votes, temporarily reducing CRV inflation and creating new incentives. Egorov and the team increased oversight to regain user trust and collaborated with white-hat hackers to recover funds. The Curve ecosystem significantly recovered throughout 2024. In October, the first crvUSD-based yield product, scrvUSD (Savings crvUSD), was introduced. This new stablecoin offers interest to its users and attracted over $20 million in deposits in its first month.

2025: As of October 2025, CRV coin price is trading around $0.7.

Why is the Curve DAO Token (CRV) Important?

There are many factors that distinguish the Curve DAO Token from its peers and make it a critical asset within DeFi. So, let's summarize the benefits of the CRV token:

A Model Focused on Stablecoin Liquidity

Curve Finance enables trading of assets of the same value (especially stablecoins pegged 1:1) with minimal price slippage. This structure ensures almost no slippage even in large stablecoin transactions, making Curve indispensable for stablecoin trading. It also provides low-slip pools for liquid staking tokens like stETH, ensuring efficient trading of these assets.

Governance Power and Community Control

CRV holders have a say in decisions that shape the future of the Curve protocol. The Curve DAO governance model utilizes community votes on a wide range of issues, from pool parameters and transaction fees to new network integrations and treasury spending. In the DeFi ecosystem, protocols like Yearn and Convex attempt to influence veCRV votes by collecting CRV. This further increases the importance of CRV in DeFi.

veCRV system (vote-escrowed CRV)

Users who lock their CRV tokens for a certain period receive veCRV in return. This system rewards long-term commitments. The longer the lockup period, the greater the user's voting power. veCRV holders not only have voting rights but also the right to share in transaction fees and receive a "boost" (yield increase) in liquidity mining. For example, a user who holds a sufficient amount of veCRV can increase their CRV rewards in pools by up to 2.5 times. This makes long-term Curve participation quite attractive.

Revenue sharing and yield opportunities

Curve distributes half of the platform's transaction fees to veCRV holders. This allows users who lock their CRV to earn passive income. CRV is also central to many yield farming strategies. Users who provide liquidity receive a share of transaction fees and CRV rewards. This system both incentivizes users and maintains Curve's strong liquidity.

DeFi Integrations and Ecosystem Impact

Curve has become an infrastructure protocol in the DeFi world. Projects like Yearn Finance, Convex Finance, StakeDAO, Frax Finance, and Lido are building their products around Curve pools. For example, Yearn vaults channel user funds to Curve and collect CRV rewards, while Convex allows users to leverage CRV without locking their CRV. Thanks to these integrations, both the liquidity and the usage area of CRV have significantly expanded.

A New Use Case with crvUSD

The Curve stablecoin, crvUSD, launched in 2023, has added new functionality to CRV. Now, users can borrow crvUSD using CRV or other collateral and utilize this stablecoin in various DeFi strategies. The success of crvUSD moved Curve from being just an exchange into the lending arena. This increased demand for CRV and protocol revenues.

Liquidity Mining Incentives

CRV is the primary reward token awarded to users who provide liquidity to pools on Curve. When a user adds assets to pools like 3pool, they receive both a share of transaction fees and CRV incentives. This model played a key role in Curve's growth. Many investors accumulated CRV by providing liquidity and, over time, became influential in the protocol's governance.

Curve Finance Ecosystem and Technical Infrastructure

Curve Finance operates under the hood with a highly innovative automated market maker (AMM) algorithm. This algorithm is customized with the StableSwap model that gives Curve its name. Unlike Uniswap's constant product formula, Curve uses a combination of constant sum and constant product formulas. This hybrid structure maintains a 1:1 value balance of stablecoins while maintaining a relatively flat price curve. This means that when the assets in the pool are similar in value, even large transactions don't significantly impact the price. As a result, users can execute high-volume stablecoin swaps with minimal slippage. For example, in the popular 3pool (DAI/USDC/USDT) pool, even multi-million dollar transactions barely disrupt the price balance.

Each Curve pool consists of assets of similar value. The most well-known example is 3pool, but there are also 2-pools (e.g., renBTC-WBTC) and 4-pools. Curve expanded this model over time, developing a new structure called a metapool. Metapools link the liquidity of a new token to one of Curve's main pools. This way, that token benefits from the main pool's liquidity, creating a deep market. For example, the sUSD metapool integrates with 3pools, enabling high-liquid exchange of sUSD against DAI, USDC, and USDT. V2 pools, introduced in 2021, include improvements optimized for more volatile assets (e.g., ETH and wBTC).

Curve is now active not only on Ethereum but on many blockchains. It operates on networks such as Polygon, Arbitrum, Optimism, Base, Avalanche, BNB Chain, and Fantom. This cross-chain structure (cross-chain expansion) has been gradually implemented since 2021. For example, users who want to avoid the high transaction fees on Ethereum can choose Curve versions on Polygon or Arbitrum. Curve distributions across different networks operate on the same principle, and CRV incentives can be shared across networks. The community is even discussing the idea of a Cross-Chain DAO (xDAO) to consolidate governance across these different chains. This has transformed Curve from an Ethereum-based exchange into a multi-chain DeFi infrastructure.

A key component of Curve's technical structure is its stablecoin, crvUSD. This token is based on the Collateralized Debt Position (CDP) model. Users can lock their collateral, such as ETH, stETH, or wBTC, into a smart contract and issue crvUSD in return. While this system is similar to MakerDAO's DAI model, Curve uses a specialized mechanism called LLAMMA (Lending-Liquidating AMM). LLAMMA gradually pays off the loan by selling collateral as the collateral ratio begins to decline, preventing users from liquidating suddenly. This provides a safer and more predictable experience for borrowers. With crvUSD, Curve is no longer just a DEX; it's also a lending platform. The scrvUSD product, introduced in 2024, offered additional income by earning interest on crvUSD balances.

Security-wise, Curve is one of the most audited protocols in the DeFi ecosystem. Companies like Trail of Bits, Quantstamp, MixBytes, and ChainSecurity have conducted numerous audits. The Curve team also runs a bug bounty program that rewards developers who identify potential vulnerabilities. Following incidents like the DNS attack in 2022 and the Vyper vulnerability in 2023, the team further tightened its security processes. Especially after the Vyper attack, legacy contracts were disabled, and the frequency of audits was increased. Despite all the risks, Curve, which has long managed billions of dollars in assets, has gained a relatively reliable position in the DeFi world thanks to its substantial security experience and strong intervention track record.

In short, Curve Finance's infrastructure: Its StableSwap algorithm, unique to stablecoins, stands out with its multi-chain deployment, collateralized crvUSD system, and rigorous auditing processes. This structure has made Curve not only an exchange but also one of the core liquidity infrastructures of DeFi. Today, many projects leverage Curve's pools and oracle data to maintain stablecoin balance and ensure price stability.

Curve DAO and Governance Model

Curve DAO is a truly community-driven, decentralized, autonomous organization. This means that control of the Curve protocol and all major decisions are determined by the votes of CRV holders. Each CRV holder has a say in the protocol's governance based on the voting power they gain by locking their tokens. Despite being referred to as the "central bank of DeFi," Curve is governed by the community, independent of a central authority. For example, the CRV reward ratios (gauge weights) of pools within Curve are determined through regular votes. The community decides how much CRV incentive should be allocated to each pool, thus increasing liquidity flow to pools with higher rewards.

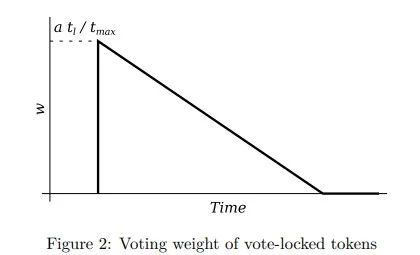

At the heart of Curve's governance model is the veCRV (vote-escrowed CRV) system. CRV holders can lock their tokens for a desired period (between 1 week and 4 years). In return, they receive veCRV based on the lockup period. veCRV is non-transferable; it simply represents voting power. This design rewards long-term participants rather than short-term investors. For example, someone who locks up for four years earns the maximum (1:1) veCRV, while shorter lockups experience a proportional decrease. veCRV holders have three key privileges: the right to participate in governance votes, receive a share of transaction fees, and receive a boost—an extra return—on liquidity mining. This model introduced Curve's "locked vote" system to the DeFi world and has become a model for many projects.

While some, such as Binance CEO CZ, advocate for token burns, Curve founder Michael Egorov and many DeFi developers argue that locking up tokens is more effective, both reducing the supply and strengthening governance.

Convex Finance holds a unique place in the Curve ecosystem. Convex is a protocol that allows users to benefit from the benefits of veCRV without actually locking up their CRV. When users stake their CRV on Convex, Convex locks these tokens in its name and issues them cvxCRV in return. This allows users to gain both boost benefits and revenue sharing without worrying about lockup periods. This model proved so popular that Convex held a significant portion of Curve's total veCRV. This gave rise to the competition known as the "Curve Wars." Convex, Frax, and similar protocols, with their significant veCRV power, began voting to channel more CRV emissions into their preferred pools. This process kept CRV demand high and shaped Curve's liquidity incentives according to market dynamics.

The Curve DAO's governance process is conducted through an open forum and voting system with thousands of participants. Discussions generally take place on the Curve Governance Forum; once proposals mature, they are put to a vote as a CIP (Curve Improvement Proposal). Accepted proposals are implemented directly within the protocol via smart contracts. The Curve DAO has become one of DeFi's largest communities, with tens of thousands of active participants. Transparency is a fundamental principle in decision-making. For example, in 2022, when a project called Mochi attempted to manipulate the voting system, the community immediately intervened, neutralizing the pool's incentives through extraordinary voting.

Curve's Developers and Community

The key figure behind Curve Finance is Michael Egorov, a Russian-born physics PhD. With an extensive background in software and cryptography, Egorov served as CTO of the decentralized data privacy project NuCypher before joining Curve. After noticing the inefficiency of stablecoin exchanges in 2019, he developed the StableSwap formula and laid the foundation for Curve. With the protocol's launch in January 2020, a completely new era in DeFi began. Egorov spearheaded Curve's technical infrastructure and emerged as a leader who prioritized community governance. Although Egorov's credit for Aave came to the fore following the hack in the summer of 2023, this further highlighted his influence in the ecosystem. As of 2025, Egorov remains active in the Curve ecosystem and is also working on a new AMM model called Yield Basis, which aims to mitigate volatile losses.

Curve's development team, led by Egorov, consists of numerous independent developers and open-source contributors. Initially a small team, the project has grown with the addition of developers from the community. Numerous contributors have joined the process, developing interfaces, testing smart contracts, and integrating new pools. The Curve team always takes a cautious approach when introducing innovations: first, security audits are conducted, then they are tested on the testnet, and finally, they are pushed to the mainnet by a community vote. This prioritizes security and stability.

This ensures that security and stability are always prioritized.

The Curve Ecosystem Fund, launched at the end of 2020, has paved the way for community-funded projects. This fund supports the promotion of new pools, security bounties, research projects, and development efforts.

On the community side, the Curve DAO boasts a large and active participant base. Every week, heated discussions take place on various topics in the forums; CRV holders express their opinions, and while disagreements sometimes arise, the outcome is always determined by community vote. Participants include individual investors as well as founders of major protocols. For example, Yearn Finance founder Andre Cronje was an active Curve supporter during 2020–2021 and popularized the concept of "Curve Wars." The Convex Finance and Frax Finance teams also regularly participate in Curve votes. This has made the Curve forums a virtual hub for discussion and bargaining in the DeFi world.

Collaborations have also played a significant role in Curve's success. Thanks to the Yearn Finance integration, Yearn vaults can earn returns from Curve pools. The partnership with Lido Finance enabled stETH/ETH liquidity to be pooled within Curve. Aave determines stablecoin interest rates using the rates in Curve pools. Even during the CRV liquidation crisis in 2023, the Aave and Curve communities worked together to resolve the issue. Frax Finance manages FraxBP, one of Curve's largest pools, and Curve has played a significant role in the success of its stablecoin, FRAX.

The community isn't solely profit-focused; it's open to innovation. Throughout 2022 and 2023, DAO forums discussed numerous ideas, including cross-chain governance, CRV systems integrated with NFTs, and new AMM algorithms. While not every project materialized, Curve discussions played a guiding role for the DeFi industry. For example, the "liquidity gauge" system and the "vote-lock" model were later adopted by projects like Balancer.

The Vote-lock model is also included in CRV's whitepaper

CRV Token Economics

One of the most important factors determining the long-term success of a crypto project is its token economics. CRV tokenomics was created with a long-term plan to support Curve Finance's growth.

The total supply of CRV was initially set at 3.03 billion, but this amount was not released at once. Curve planned a declining emission schedule spanning approximately 300 years. According to this schedule, the amount of new CRV entering circulation each year gradually decreases. At launch in August 2020, there was almost no CRV in circulation; rewards were distributed at a high emission rate in the first year. The production rate was gradually reduced in subsequent years. By 2025, approximately 1.9 billion of the total supply of 3.03 billion had been produced, of which approximately 1.1 billion were actively traded. The remainder is still locked or vested.

CRV distribution was planned from the outset to be fair and incentive-driven. The percentages were as follows:

• 62% – Liquidity providers (as rewards for those who fund Curve pools)

• 30% – Community reserves and ecosystem incentives (strategic partnerships, development funds, emergency budgets)

• 3% – Employees (with a 2-year vesting period)

• 5% – Founders and early investors (with a 2-4 year vesting period)

This distribution allowed the majority of CRV to be distributed to the community through liquidity mining in the early years. The gradual release of team and investor shares prevented early market selling pressure.

While CRV is inherently inflationary, this inflation was designed to decrease annually. Initially, approximately 300 million CRV were produced annually; this amount has been decreasing by an average of 15% annually. While more than 1 CRV was produced per second in 2021, this rate has decreased significantly by 2025. Reaching the full supply will take a very long time, likely reaching the 2100s. The logic behind this model is to attract liquidity with high rewards in the initial stages and to maintain the token's value by limiting supply growth in subsequent years.

Another notable aspect of the CRV economy is the burn and buyback mechanisms. CRV is not a token that is constantly burned; on the contrary, its supply increases over time. However, Curve DAO has taken steps to use protocol revenues to support CRV value. With a decision made at the end of 2020, 50% of transaction fees began to be channeled into the DAO treasury. These revenues were used to buy back 3CRV tokens from the market and distribute them to CRV holders. Further strengthening this model and burning a portion of the collected 3CRV were discussed in 2022.

Michael Egorov emphasized in his statements in 2023 that even without a direct CRV burn mechanism, the CRV lockup system effectively produces the same effect. Long-term lockups support the token price by reducing the circulating supply. Proposals such as further reducing CRV inflation in the future or making direct market purchases with the proceeds are still being discussed within the Community.

Frequently Asked Questions (FAQ)

Below are some frequently asked questions and answers about the Curve DAO Token:

What is the Curve DAO Token (CRV) and what does it do?: CRV is the governance and rewards token of the Curve Finance protocol. CRV holders can vote in the protocol, earn liquidity mining rewards, and receive a share of transaction fees through CRV. In short, CRV provides both governance power and incentives within the Curve ecosystem.

When and by whom was Curve DAO founded?: The Curve protocol was founded in January 2020 by Michael Egorov, a Russian-born software developer with a PhD in physics. The Curve DAO and the CRV token launched in August of that year. The official launch date of Curve DAO is considered to be August 14, 2020.

Which blockchains does Curve Finance work on?: Curve was originally developed on Ethereum but has evolved over time into a multi-chain structure. Today, Curve: Polygon is active on many different networks, including Arbitrum, Optimism, Base, Avalanche, BNB Chain, Fantom, Harmony, and xDai. Users can exchange stablecoins through Curve interfaces on these networks. This has made Curve one of the most widely used multi-chain DEX platforms in the DeFi world.

What is the veCRV system?: veCRV (vote-escrowed CRV) is a special governance token obtained by locking CRV tokens for a specified period. Users can lock their CRV for any period, from 1 week to 4 years. The longer the lockup period, the more veCRV is earned. veCRV holders have the right to participate in voting in the Curve DAO, receive revenue shares from transaction fees, and earn boosts (increased returns) on liquidity mining rewards. This system forms the basis of Curve's long-term participation reward structure.

Is Curve Finance safe?: Curve is one of the most regulated and widely used protocols in the DeFi space. Its smart contracts have been audited numerous times by firms like Trail of Bits and Quantstamp. While generally operating stably since 2020, there was a DNS attack in 2022 and a hack caused by the Vyper vulnerability in 2023. The team responded quickly to these incidents, recovering a large portion of user funds. Today, Curve is considered a "vetted but risky" protocol, as smart contract risk cannot be completely eliminated in the DeFi world.

What is crvUSD?: crvUSD is a stablecoin launched by Curve Finance in 2023, pegging its value to $1. Users can mint crvUSD by locking their ETH, wBTC, or similar collateral into smart contracts. What distinguishes crvUSD is its special liquidation mechanism called LLAMMA. This system gradually sells the position when the collateral value begins to decline, preventing sudden liquidations. This provides a more stable and secure borrowing experience for users.

Don't forget to follow our JR Crypto guide series for the latest developments in the Curve DAO Token and DeFi world.

#what is curve dao token#what is crv#curve dao token#what is curve finance#crv coin price#what does crv coin do#curve dao governance#curve dao hack#curve dao history

Do you have any questions?Feel free to send us your questions or request a free consultation.